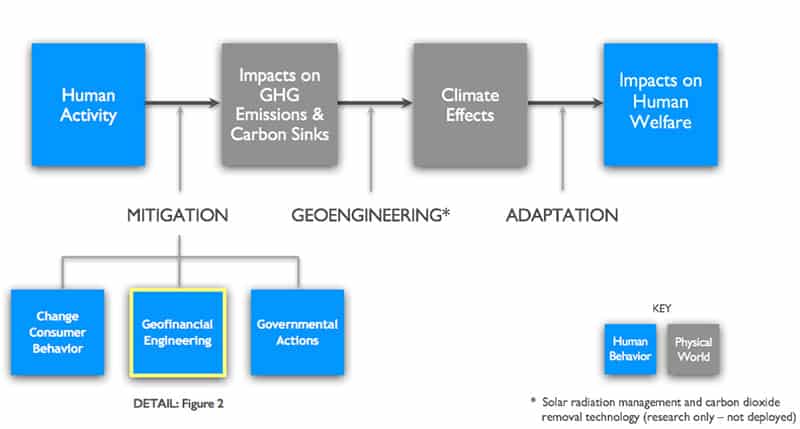

The recent withdrawal of the US from the Paris Climate Agreement has injected global policy with a renewed sense of uncertainty over the outlook for regulation of greenhouse gas emissions. But even if the US were to keep its commitment, the Paris goals are not enough to avoid substantial, worldwide climate impacts.

We need additional levers beyond governmental policy to improve the odds of averting catastrophic climate change. Financial market pressure is already playing a central role. Yet, while long-term institutional investors such as sovereign wealth and pension funds are integrating climate-change considerations into their investment decisions, such efforts fall well short of the climate challenge. One of the main reasons for this shortfall is the difficulty of connecting specific investment assets, such as stocks of publicly traded companies, to the negative consequences of companies’ actions. However, if such environmental externalities can be both quantified and attributed to a given company or asset in near real-time, then asset prices may begin to reflect the costs of irresponsible behaviours more accurately.

With that in mind, we propose a new approach: geofinancial engineering. This uses financial tools and scientific knowledge to leverage the capital markets to change human impact on the physical world and improve the odds of averting catastrophic climate change. As a market-based initiative, geofinancial engineering can operate independently from government action or can amplify the effectiveness of market-based regulation like carbon pricing or emission penalties. Given the recent policy swing from the science-driven Obama administration to the climate denialism of the Trump administration, policy-independent mechanisms are particularly timely.

As a mitigation strategy, geofinancial engineering aims to preemptively reduce the prevalence of behaviours that cause the most environmental damage – such as extracting and burning high-carbon fossil fuels, deforestation, methane-intensive agricultural practices, and loss of non-renewable water sources (figure 1).

Geofinancial engineering aims to improve climate outcomes by increasing the cost of capital for companies engaged in harmful behaviour, and by reducing the cost of capital for more climate-resilient options (figure 2).

As we mentioned, many long-term institutional investors are already integrating climate-change considerations into their investment decisions. However, hedge funds and quantitative (or algorithmic) trading systems, which often buy and sell in a matter of milliseconds are, with few exceptions, inherently climate agnostic. Although these now-pervasive strategies focus more on signals than fundamentals of underlying securities, they do not take real-time signals linked to the environment into account. Such signals either aren’t accessible in a systematic and standardized way or simply aren’t connected to the applications used by the trading community.

Making relevant, real-time environmental risk data readily available to climate-agnostic traders and investors – both automated and human – could shift financial market sentiment against behaviour that damages climate stability. At the same time, such transparency could enable those traders and investors who decide to use the new datasets proactively to avoid climate-related market risks and seize opportunities. Through this mechanism, environmental researchers can spur action by traders and investors and accelerate shifts in the global capital markets, where approximately $350 billion in equities are traded daily.

Satellite data on methane emissions by publicly traded fossil-fuel producers and utilities is one promising example. A suite of information aggregated from current and planned public satellites has the potential to detail methane flaring and venting activity at a fine enough spatial and temporal scale to allow for a nearly real-time assessment of methane emissions (figure 3). Venting or flaring (burning) methane accelerates climate change, the global impacts of which are well known and documented. Venting is particularly problematic because methane is 86 times more potent than carbon dioxide as a greenhouse gas and venting accounts for about a third of global methane emissions.

Several existing remote sensing satellites are capable of measuring both methane flares and venting. In particular, NOAA’s VIIRS satellite can measure flaring at a sufficiently high resolution to track daily changes by flare site and link it directly to the company running the facilities. And private ventures such as Planet Labs’ satellite constellation can provide even higher resolution data. Venting is harder to measure since spectrometers must capture the non-visible parts of the spectrum. Planned and proposed satellites, particularly the German EnMAP satellite (set for launch in 2019), may for the first time provide a global dataset at the frequency and resolution needed to pinpoint venting emissions by source. Local tracking also is available using spectrometers from airplanes and drones, as well as other sensors on ground vehicles. Collated together, these sources can build a state-of-the-art, real-time dataset that provides detailed information on all five of these key methane indicators – consistent flaring, consistent venting, change in methane flaring practices, change in methane venting practices and large methane venting anomalies (see figure 3). By assigning these emission data to the spatial location of specific company assets, market players can act on changes in both long-term behaviour and short-term anomalous emission activity.

Up to the minute

Delivering environmental risk data to investors, human traders and algorithmic trading systems – in near real-time before it is generally known – in a format that seamlessly integrates with their workflow would pull the geofinancial engineering lever.

A successful system must create transparency, preferably in near real-time, since knowing about intangible disasters before others is what makes the information actionable to traders. Knowing first –by a day, an hour or a few hundred milliseconds – can deliver the information advantage they seek.

Increasingly, such algorithmic strategies seek trading and investment signals from non-financial sources to gain an advantage, however slight. In this context, environmental researchers can trigger shocks in risk perceptions or confidence around investment in fossil fuels or other damaging activities. They can do so by delivering timely empirical data and analysis to machine-readable apps and other analytic tools, and incorporating them into the financial terminals that drive these apps (figure 4).

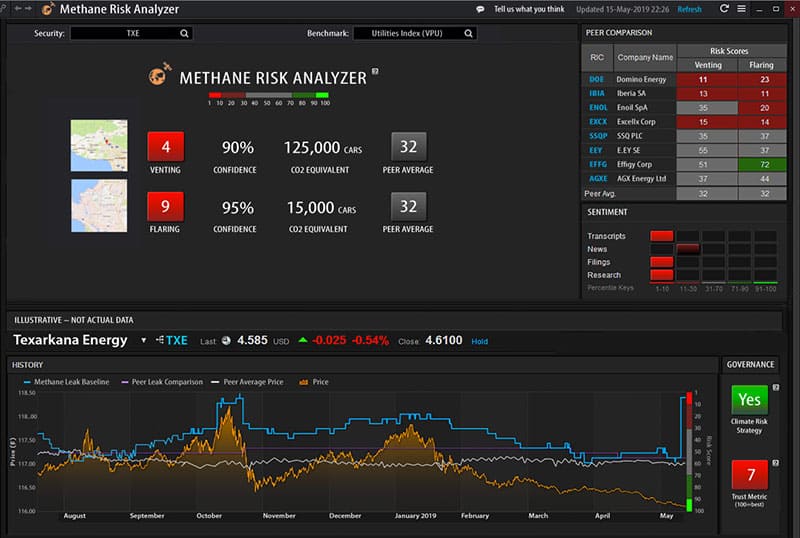

A hypothetical methane risk analyser (figure 5) illustrates how real-time methane risk data on a specific publicly traded company might appear on a (climate-agnostic) trader’s terminal in the near future. When a new anomaly is detected, this information would be fed into the terminal and immediately affect the risk score, allowing traders to react given the size of the leak, past company behaviour, and the risk scores of its peers. Such an app could be programmed to include a notification system that triggers buy/sell trading decisions given pre-selected risk thresholds.

Though we are characterizing the benefits of a trading-based approach to changing corporate behaviour, there are potential side effects. Privatizing benefits of greenhouse gas reduction is a key strength of the geofinancial engineering approach because it drives uptake in a large and diverse marketplace, and we need large-scale transformation to prevent catastrophic climate change. But this may also have downsides, including potential further concentration of financial gains, and shifting power in the carbon markets away from socially-minded investors and policy makers. At the Geofinancial Engineering Initiative we propose a collaborative civic-oriented “open data” approach to mitigate some of these concerns.

Another important caveat concerns the effectiveness of geofinancial engineering. Specifically, the newsworthiness or public perception of certain greenhouse gas emissions may not correlate well with the climate impact of different greenhouse gas sources. For instance, venting is far worse than flaring since unburned methane has higher impacts than burned methane, but flaring means more fire, which could be more “newsworthy” and viewed by traders as more likely to move the short-term market. In other words, information may not move the market for the right reason or may incentivize the wrong things. In the same vein, a focus on publicly traded “super emitters” could overlook cumulative venting by numerous, smaller emission sources, as well as the many private- and state-owned “super emitters” that are shielded from financial market pressure for transparency and accountability. In those cases, engagement may be the best and only option.

Although climate change as an investment consideration is moving into mainstream asset management and institutional investing, the financial market sectors that now generate most of the daily trading volume – hedge funds and algorithmic trading systems – simply do not include it.

Our proposed concept takes the next step: real-time, satellite-captured information relevant to climate change is linked to specific assets and fed into the financial markets. This “real-time” pricing of externalities can apply to both climate-motivated and climate-agnostic traders and investors as long as there are market signals that impose price penalties on the heightened liabilities of corporations engaging in climate-irresponsible behaviours.

Geofinancial engineering would benefit from further research and initial testing to improve information collection, analysis, and dissemination. Investments in improved remote and local sensing options should enhance the ability of markets to respond to real-time information from geofinancial engineering tools. Given the value of improved temporal detail and spatial accuracy, for example, one could imagine a cluster of nanosatellites such as the private Planet Labs constellation that includes spectrometers similar to those of EnMAP or other proposed satellites. This would take real-time, accurate information on greenhouse gas emissions to the next level. Careful consideration of the indirect effects of geofinancial engineering is also critical, particularly since the social need for greenhouse gas emission reduction is large and pressure to take action could and should intensify in the near future.

Geofinancial engineering is now moving from the drafting board to the lab. For example, testing of methane emissions data by traders will begin shortly to determine if data offer actionable trading insights (see Geofinancial Engineering Initiative). Exploration of environmental remote sensing data other than methane and complementary information on supply chains and asset-level data for attribution is also under way.

Longer term, given the declining cost of launching satellites, privately funded consortia consisting of NGOs, academic institutions, foundations, and climate impact-oriented tech firms like Google, Tesla or SpaceX might make such information publicly available. If coupled with publicly funded satellite data and a freely-accessible platform such as the one illustrated in figure 5, then all investors, traders and stakeholders, regardless of their capital resources, could leverage this information to make environmentally sound decisions – and improve climate outcomes.

- The full version of this article has previously been published by the Journal of Environmental Investing in volume 8 and can be obtained at www.thejei.com.